Monopolies, Duopolies, and the Illusion of a ‘Free Market’

How regulatory capture, network effects, and monopoly stocks quietly shape the portfolios of affluent investors.

Fundamental Analysis and Technical analysis contained in this post was performed by Andrew Jodice of Markets, Liberty, & Discipline. He’s studied and blends Al Brooks’ theory, Richard D. Wyckoff’s theory, and Charles H. Dow’s theory to conduct his analysis, and implements Al Brooks’ strategy to execute trades.

")

The chart that kicked this off

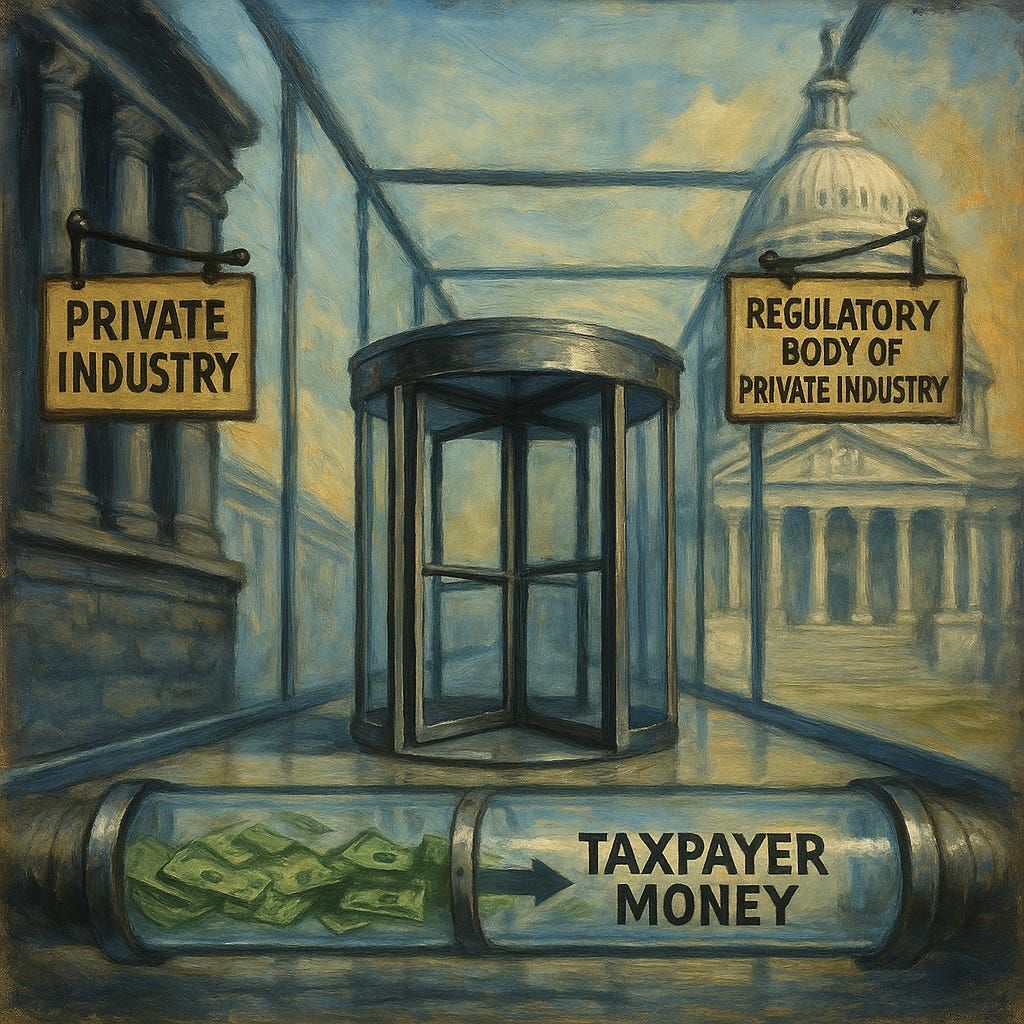

At the top of this post is a political-cartoon: a glass hallway between Washington, D.C. and Wall Street, a revolving door in the middle, and a clear pipeline labeled “Taxpayer Money” flowing one way.

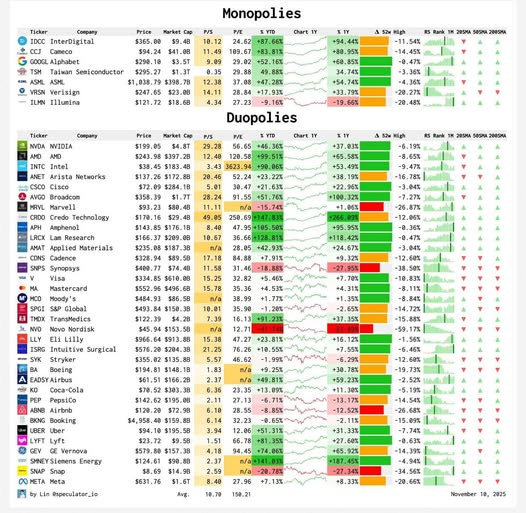

Now pair that image with the table of “Monopolies” and “Duopolies”:

Monopolies

Search: $GOOGL

Semi Fabs: $TSM

Wireless IP: $IDCC

Lithography: $ASML

Uranium Refining: $CCJ

Domain Registry: $VRSN

DNA Sequencing: $ILMN

Duopolies

GPUs: $NVDA / $AMD

CPUs: $AMD / $INTC

Networking: $ANET / $CSCO

ASICs: $AVGO / $MRVL

AEC: $CRDO / $APH

Etch Equipment: $LRCX / $AMAT

Chip Design Software: $CDNS / $SNPS

Credit Cards: $V / $MA

Credit Rating: $MCO / $SPGI

Organ Transport: $TMDX / $XVIVO

Weight-Loss Drugs: $NVO / $LLY

Surgical Robots: $ISRG / $SYK

Aircrafts: $BA / $EADSY

Coke: $KO / $PEP

Mobile OS: $AAPL / $GOOGL

Travel: $ABNB / $BKNG

Rideshare: $UBER / $LYFT

Gas Turbines: $GEV / $SMNEY

Social Media: $META / $SNAP

If you are a high-income professional trying to compound wealth, this list is basically a cheat-sheet of monopoly stocks and oligopoly stocks that dominate their lanes.

But it also raises an uncomfortable question.

If this is what a “free market” looks like, what exactly are our antitrust and securities regulators doing?

Monopolies vs. “functional monopolies”

In a standard economics text, a monopoly is a single firm that faces no close substitutes and can meaningfully set prices. K-State Libraries+3Investopedia+3Economics Help+3

An oligopoly is a market where just a few large firms dominate output and pricing power. Federal Reserve Education+4Investopedia+4Wall Street Prep+4

Most of the names in our table are not literal, textbook monopolies. Instead, they are what I will call functional monopolies or tight oligopolies:

They control essential infrastructure, standards, or intellectual property.

They operate in markets where barriers to entry are high.

They capture the lion’s share of the profit pool, even if a few smaller players exist.

If you want to go deeper on the formal definitions, good starting points are:

A tour of the chokepoints

Let us walk through a few of the most important chokepoints on the list, because this is where structural advantage and portfolio risk collide.

True chokepoints in the global economy

ASML ($ASML) – EUV lithography

ASML is effectively the sole supplier of extreme ultraviolet (EUV) lithography machines needed to manufacture the most advanced chips. ASML+2The Guardian+2

Without ASML tools, the entire high-end semiconductor stack — including NVIDIA GPUs and Apple’s latest processors — does not exist. For an affluent investor, this is the definition of a “must-own chokepoint,” but also a massive single-point risk.TSMC ($TSM) – leading-edge foundry

Taiwan Semiconductor dominates leading-edge production for advanced logic nodes. Alternative foundries exist, but in the 3–5nm class, TSM’s ecosystem, yield, and tooling lead give it quasi-monopoly power at the bleeding edge.Verisign ($VRSN) – .com/.net registry

Verisign operates the registry for the .com and .net domains under long-term agreements, giving it a unique position in the backbone of the internet.Visa ($V) and Mastercard ($MA) – card networks

Outside China, Visa and Mastercard process the overwhelming majority of global credit-card transactions — estimates put their combined share around 90% of card payment volume. The Street+3Quartr+3Fortune+3For merchants and consumers, they are essentially the default rails.

Moody’s ($MCO) and S&P Global ($SPGI) – credit ratings

Together with Fitch, they dominate sovereign and corporate credit ratings, with estimates of 95–99% global market share in some segments. Investopedia+2ScienceDirect+2

Their opinions are embedded into regulations, collateral rules, and investment mandates.

For a wealthy investor building a core equitable portfolio, these names are not just “good businesses” they are systemic nodes. That is precisely why they deserve both attention and skepticism.

Winner-take-most digital platforms

Apple ($AAPL) and Alphabet ($GOOGL) – mobile OS and app stores

iOS and Android are the only mobile operating systems that matter at global scale. The app ecosystems around them exhibit strong network effects — each new user and developer makes the platform more valuable. Wall Street Prep+4Investopedia+4Harvard Business School Online+4Meta ($META) and Snap ($SNAP) – attention markets

Together, they control huge slices of mobile attention and ad inventory, particularly among younger demographics. Businesses that target affluent consumers — luxury travel, premium credit cards, high-end retail — all compete for real estate on these platforms.NVIDIA ($NVDA) and AMD ($AMD) – GPUs and accelerators

In discrete GPUs and general-purpose accelerators used for AI and high-performance computing, NVIDIA dominates with AMD as the primary alternative. Custom ASICs and cloud-provider chips are emerging, but for most enterprises deploying AI today, “GPU” still effectively means “NVIDIA.”

Niche but powerful oligopolies

A few pairs on the list live in narrower, but highly lucrative niches:

ISRG / SYK – surgical robots

TMDX / XVIVO – organ transport technologies

BA / EADSY – large commercial aircraft

These are textbook oligopoly industries: high capital costs, intense regulation, and long product cycles that favor a small club of big players. Investopedia+2Wall Street Prep+2

For investors with disposable income and a long horizon, these can behave like “hidden monopolies” inside healthcare and industrials.

How did we end up here?

Blaming everything on lazy or corrupt regulators is emotionally satisfying but analytically weak. Three structural forces explain most of what we see.

1. Network effects and data compounding

Digital platforms and payment networks benefit from network effects — the more users and transactions they handle, the more valuable they become to everyone in the network. Wall Street Prep+4Investopedia+4Harvard Business School Online+4

That is why:

Developers build for iOS and Android, not fringe operating systems.

Merchants accept Visa and Mastercard by default.

Advertisers pay up for Meta and Google’s reach and targeting.

Once the flywheel spins, it becomes exceptionally difficult for a new competitor to dislodge the incumbent.

2. Scale economics and capital intensity

Industries like semiconductors, aerospace, healthcare robotics, and gas turbines are brutally capital-intensive. The up-front cost of fabs, lithography tools, certification, and R&D is measured in billions.

In such environments, economies of scale naturally push toward a small set of survivors — exactly what we see with TSMC, ASML, Boeing/Airbus, and a handful of med-tech platforms. The Times of India+2Tom’s Hardware+2

3. Regulation that locks in incumbents

This is where the thumbnail’s “Taxpayer Money” pipe becomes important.

Credit ratings from the “Big Three” are written directly into regulations and capital requirements. Investopedia+2SSRN+2

Card-network rules and settlement standards make it extremely hard for alternative rails to gain traction, even when technology exists. Quartr+2Payments Dive+2

Compliance costs and licensing regimes favor those large enough to amortize the overhead.

When rules are written around today’s giants, tomorrow’s competitors must fight both economics and regulation. That is not always a deliberate conspiracy, but it looks a lot like what economists call regulatory capture — regulators gradually serving the interests of the regulated industry instead of the public. The Regulatory Review+4Investopedia+4Economics Help+4 [Theory]

So… what exactly is the SEC doing?

Here is the key nuance most headlines skip:

Antitrust enforcement — deciding whether a merger is anti-competitive or whether a platform has abused monopoly power — is primarily handled by the Department of Justice (DOJ) Antitrust Division and the Federal Trade Commission (FTC). Winston & Strawn+4Federal Trade Commission+4Government Accountability Office+4

The SEC’s mandate is narrower: policing securities markets, disclosure quality, insider trading, and market manipulation.

So if you are looking for a single villain behind concentrated industries, the SEC alone is a poor target.

That said, the revolving door shown in the thumbnail is not fiction:

Career paths routinely move from large banks, hedge funds, and mega-caps into agencies and back out again.

The same is true for senior roles at the Fed, Treasury, DOJ, and the SEC.

This pattern does not require a secret conspiracy to have real consequences. It nudges the entire system toward protecting incumbents, because rocking the boat too hard is almost never the optimal move for someone whose future earning power depends on staying in the club.

A more precise statement than “the SEC incentivizes monopolies” would be:

The current U.S. regulatory architecture, including the SEC, FTC, DOJ, and the Fed, often tolerates and indirectly reinforces winner-take-most market structures through a mix of network effects, complex rules, and regulatory capture.

Why this matters for investors

If you are reading this, odds are you already have some capital to deploy — a high-income job, stock options, or accumulated savings. The question is how to use this map of monopolies and duopolies.

The attractive side: durable cash-flow machines

From a portfolio-construction perspective:

Many of these companies earn high and persistent returns on invested capital because of their structural moats.

They can often raise prices or hold pricing during inflation and recessions.

Their brand, data, and regulatory moats make disruption slower than headlines suggest.

If you are building a core equity sleeve inside a taxable brokerage account, IRA, or trust, these are natural candidates for long-term compounders.

Hyper-relevant search phrases here would be:

“best monopoly stocks for long-term investors”

“duopoly stocks with pricing power”

“how to invest in network-effect platforms”

This post is not a screen or a model portfolio, but the list at the top is a good starting universe for further research.

The dark side: concentration and policy risk

The same features that make these stocks attractive to affluent investors also make them fragile in a different dimension:

They are exposed to regulatory and political backlash when the public mood swings toward “break up Big Tech” or “cut card fees.” Steptoe+4Quartr+4Fortune+4

Portfolios overweight these names are effectively betting that current rules and power structures will persist.

Disruption, when it finally arrives, tends to be abrupt and brutal (think telecom deregulation, or what low-cost carriers did to legacy airlines).

For high-net-worth or mass-affluent investors, the practical takeaway is simple:

Treat monopoly and duopoly exposures as risk factors as much as moats. Size them consciously, and stress-test what happens if regulation or technology tilts the board.

Where I land

When I put the chart of “Monopolies” and “Duopolies” next to the thumbnail of the revolving door and the “Taxpayer Money” pipe, a few conclusions emerge:

We do not live in a textbook free market. We live in a system of critical chokepoints run by a small group of firms with deep ties to regulators.

Network effects, scale economics, and regulatory complexity naturally push us toward winner-take-all outcomes.

The revolving door between Wall Street and Washington amplifies that tendency through regulatory capture, even without explicit corruption. study.com+4Investopedia+4Economics Help+4

For investors with disposable income, these companies are both opportunities and concentrated risks. The better you understand the structure, the less you are just passively along for the ride.

You do not have to believe in a grand conspiracy to be uneasy about this. What you do need is a clear-eyed view of where your capital is actually exposed.

So I will leave you with the same question I asked myself writing this:

Are you consciously allocating to these monopoly and duopoly franchises because you understand their power — or have you simply outsourced the decision to index funds that own them by default?

Fact vs Theory Audit

DOJ and FTC are the primary U.S. antitrust enforcers; the SEC focuses on securities regulation and investor protection. Winston & Strawn+4Federal Trade Commission+4Government Accountability Office+4

ASML is the sole supplier of EUV lithography tools used for the most advanced semiconductor nodes. ASML+2The Guardian+2

Visa and Mastercard together process the majority of card payments outside China and are widely described as a global payment duopoly. The Street+3Quartr+3Fortune+3

The credit-rating industry is dominated by Moody’s, S&P, and Fitch; regulations embed their ratings into financial rules. Cato Institute+3Investopedia+3ScienceDirect+3

Network effects and economies of scale are well-documented drivers of concentration in digital platforms and payment systems. Wall Street Prep+4Investopedia+4Harvard Business School Online+4

Theories

Labeling the companies in the opening table as “functional monopolies” or “tight oligopolies” is an analytical judgment based on market structure, not a legal designation.

Regulation that embeds today’s incumbents into rules and standards tends to reinforce their dominance and raise barriers for challengers. The Regulatory Review+3Cato Institute+3Investopedia+3

The revolving-door career incentives of regulators and industry leaders bias the system toward protecting incumbents, even without explicit corruption.

For investors, overweight exposure to these stocks is effectively a leveraged bet on the persistence of current regulatory and technological regimes.

Speculation

The exact degree to which specific agencies or individuals consciously prioritize industry interests over public interests cannot be proven from public data and remains uncertain.

The timing and severity of future regulatory backlash or technological disruption to any individual company on the list are inherently uncertain.

Legal disclaimer

This article is for educational and informational purposes only and reflects personal opinions at the time of writing. It is not investment advice, a recommendation to buy or sell any security, or a solicitation to engage in any investment strategy. Trading and investing in financial markets involves substantial risk, including the risk of total loss of capital. The majority of active traders and day traders lose money over time. You should conduct your own research, consider your individual financial situation, and consult with a qualified, licensed financial professional before making any investment or trading decisions.

Hey, great read as always. This list really highlights the problem. Do you see any effective regulatory paths forward? Brilliant work!