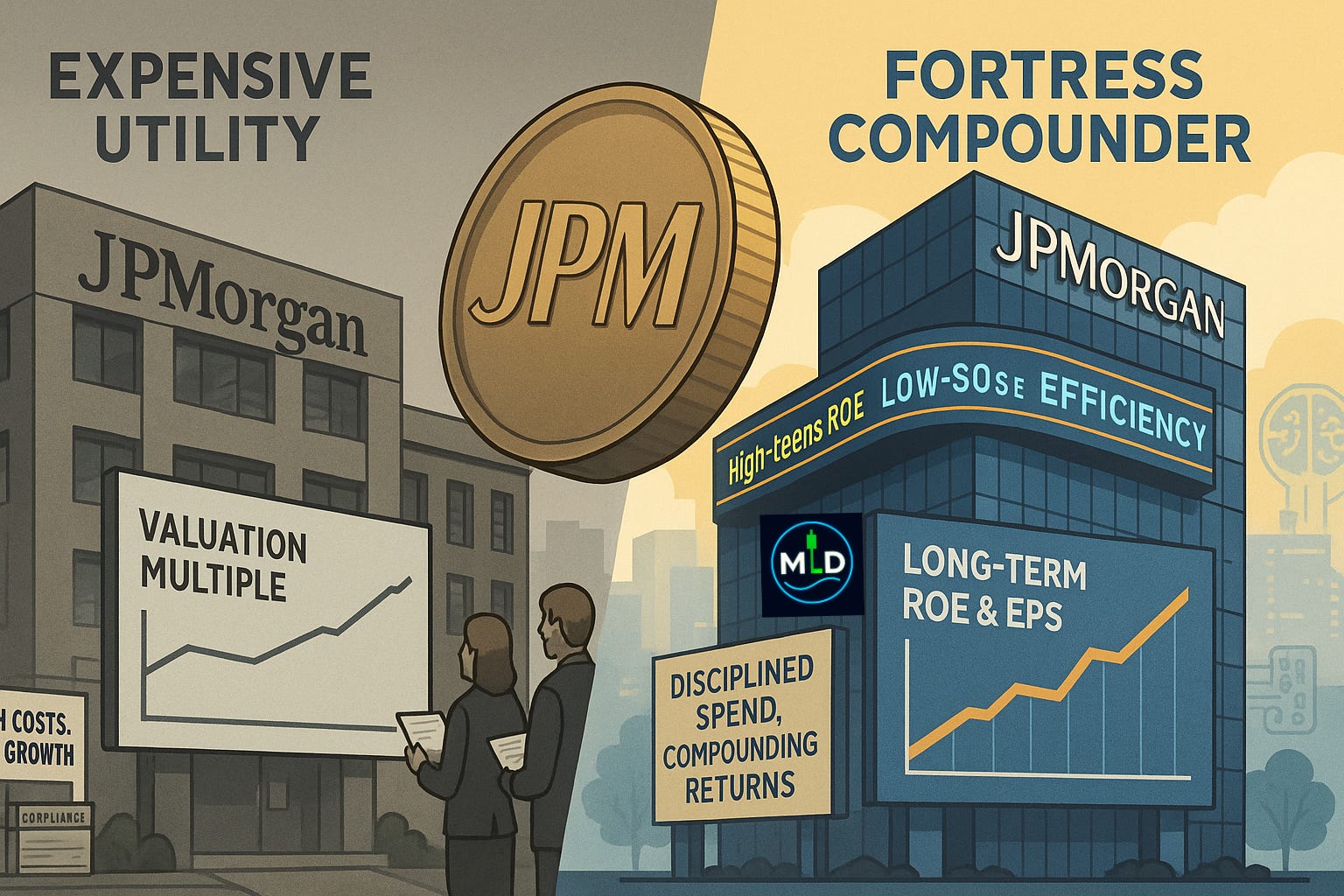

JPMorgan’s $105 Billion Warning Shot: When The “Safe” Bank Gets Repriced

JPMorgan was supposed to be the safe financial stock for portfolio's.

Fundamental Analysis and Technical analysis contained in this post was performed by Andrew Jodice of Markets, Liberty, & Discipline. He’s studied and blends Al Brooks’ theory, Richard D. Wyckoff’s theory, and Charles H. Dow’s theory to conduct his analysis, and implements Al Brooks’ strategy to execute.

Marianne Lake said one number on one stage and the stock traded like a growth name that had just missed earnings by 20%. A single slide on 2026 expenses erased nearly 5% of market cap in a day and turned a sleepy bank chart into a cliff.

This isn’t about a credit blow-up. It’s about what it now costs to run a state-sized bank in a world of sticky inflation, AI arms races, and permanent regulatory sprawl.

Let’s walk through what changed, what the market actually repriced, and where the opportunity might sit once the dust settles.

What Actually Happened To JPMorgan Stock

JPMorgan Chase dropped about 4.7% in one session, its sharpest one-day decline since early April, closing around $300.5 and finishing as the biggest loser in the Dow Jones Industrial Average. (Yahoo Finance)

The trigger was straightforward:

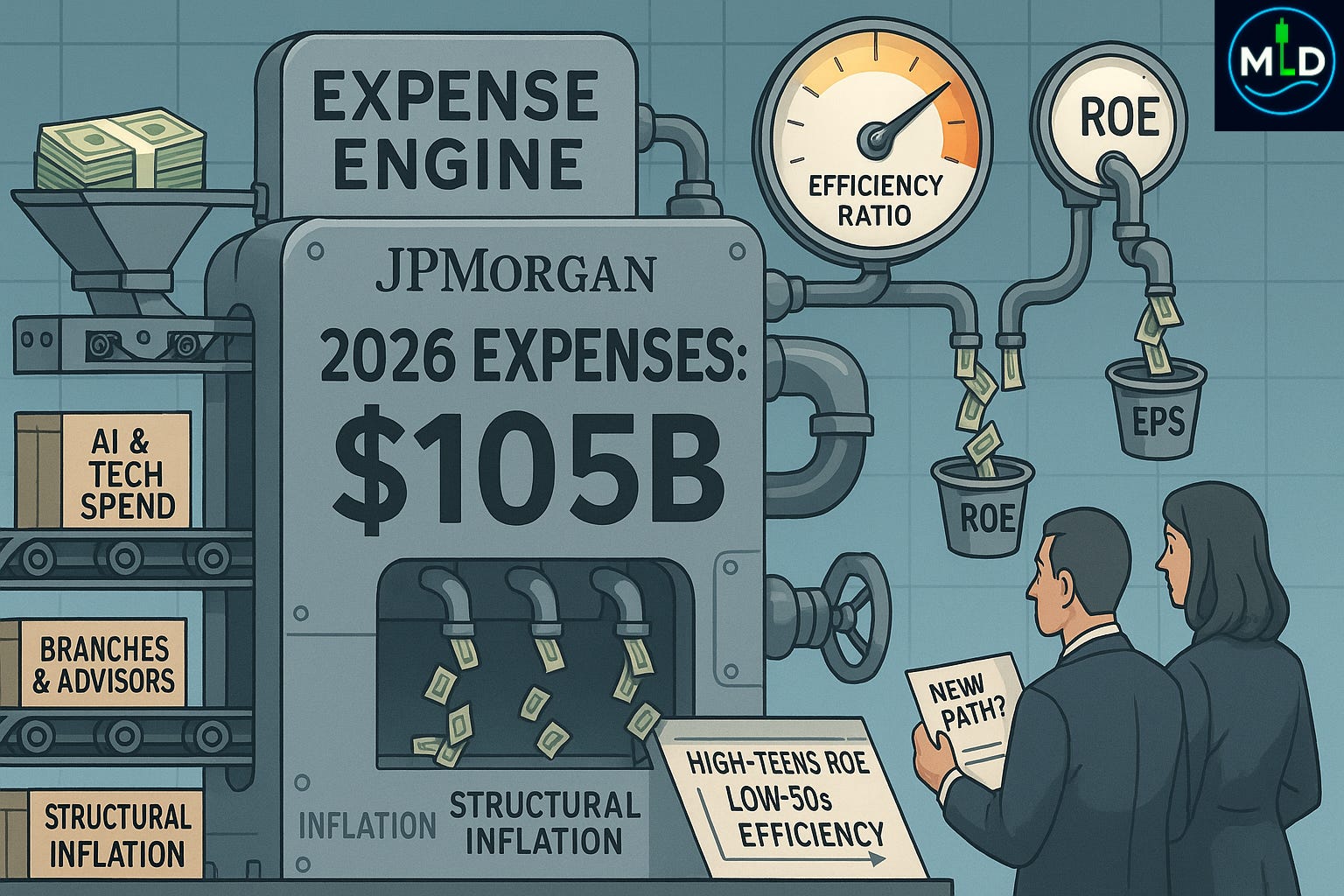

At Goldman Sachs’s U.S. Financial Services Conference, Marianne Lake, who runs consumer and community banking, said JPMorgan now expects 2026 expenses of roughly $105 billion. (Investing.com)

Wall Street had been modeling about $100–101 billion, and the bank itself is planning to spend around $95.9–96 billion this year and next. (Investing.com)

Call it a $4–5 billion surprise versus consensus and roughly 9–10% year-on-year expense growth.

Lake pointed to “volume and growth-related” costs, heavy investment in artificial intelligence and technology, more marketing and card growth, higher advisor incentives, branch expansion, and structural inflation in things like real estate. (Investing.com)

What she didn’t flag was just as important:

No new hole in credit quality.

No capital shortfall.

No downgrade-style event.

Fundamentally, the message was: JPMorgan will still earn money; it’s just going to spend a lot more to run the machine.

The chart reacted to that single sentence.

The Math The Market Ran In About 30 Seconds

Banks are simple in one way: they live and die on return on equity and their cost base.

JPMorgan has been printing elite numbers on both fronts:

High-teens ROE and around 20% return on tangible equity. (Yahoo Finance)

An efficiency ratio (non-interest expenses divided by net revenue) in the low-50% range, better than most large peers. (INDmoney)

Now layer in the new guidance:

Expense base today: about $96 billion.

Guided expense base in 2026: $105 billion.

Incremental cost: ≈ $9 billion, or roughly 9–10% growth.

Unless revenue grows at least as fast, the efficiency ratio moves the wrong way. Margin expansion flips to margin compression. That hits earnings and eventually compresses the valuation multiple.

Investors weren’t paying up for “double-digit expense growth and we’ll see what happens.” They were paying for fortress balance sheet, strong net interest income, and tight cost control at a mature franchise.

Once Lake moved one of those three legs, the premium multiple had to be re-examined. That’s what you’re seeing in that vertical blue line on the chart: a single-day repricing of the earnings path.

Why A Boring Bank Chart Turned Into A Cliff

Crowded “Safety” Trade Meets Clean Negative Catalyst

JPMorgan isn’t a niche stock. It’s:

A core holding in financials ETFs.

A heavy weight in the Dow Jones Industrial Average.

The default “quality bank” for institutions that want bank earnings without regional-bank drama. (Yahoo Finance)

Crowded longs behave badly when the narrative turns:

Long-only funds de-risk.

Factor and quant models pick up the relative weakness and pile on.

Index funds mechanically push selling pressure through the Dow and financials baskets.

Short-term traders lean into the momentum.

You don’t need panic for a 4–5% drop; you just need everyone hitting the same exit at once.

Cost Of Equity Versus Cost Of Growth

In a world where base rates are no longer zero, the cost of equity for a large bank is not trivial. If you’re going to reinvest billions instead of paying them out, those dollars have to earn more than that hurdle.

When management says “expenses will be $105 billion, not $101 billion,” the market quickly asks:

Will that extra $4–5 billion of annual spend produce incremental earnings above our required return?

Or are shareholders quietly subsidizing an AI and branch arms race?

Until there’s proof on the revenue and productivity side, the default answer is “show me,” and the stock trades down.

The AI And Growth Story Underneath The Cost Spike

Lake’s list wasn’t just “inflation and compliance.” The emphasis was on:

AI and technology build-out.

Card growth and marketing.

More financial-advisor comp.

Physical expansion of the branch footprint. (Investing.com)

Across the industry, big banks are pouring money into AI—claiming better productivity, faster decisioning, and improved risk management. Central bankers and regulators are already studying how AI in finance will reshape credit allocation and market structure.

That’s the strategic backdrop: if you don’t spend, you drift toward being a regulated utility with shrinking margins. If you do spend, you front-load pain on the expense line and hope the revenue and efficiency gains show up later.

JPMorgan is choosing to spend.

From a libertarian, market-structure perspective, this is a classic late-cycle problem: prior years of artificially cheap money helped create mega-institutions that must now invest like tech platforms just to maintain their position. The bill for that scale is coming due in the form of a bigger, stickier cost base.

Signals For Investors: What To Watch Next

Earnings Revisions Versus Price

Watch how 2025–26 EPS estimates move over the next few weeks. If the stock ends up 10–15% below its highs but EPS estimates only fall 3–5%, most of the damage will be multiple compression, not math. That’s where value-driven funds start thinking in terms of expected return rather than headlines.

Efficiency Ratio And Profitability

The key metrics going forward are the efficiency ratio and ROE:

If revenue growth, AI productivity, and card volumes keep the efficiency ratio anchored near the low-50s, the market will eventually treat this as “investing for growth.”

If expenses outrun revenue for multiple years and ROE drifts meaningfully lower, the stock will settle into a more pedestrian valuation.

Credit Quality

The true nightmare scenario isn’t just higher opex(OPEX = the running costs of the machine.) It’s higher opex colliding with a turn in credit risk rising card charge offs, consumer stress, or a broader downturn. Lake described the consumer as “somewhat fragile” but not breaking. (Investing.com) That language matters. If the data starts to echo it, the market will re-price again.

The Rest Of The TBTF Complex

Finally, watch the other too-big-to-fail banks. Early commentary already hints that peers may be forced to step up spending on tech, AI, and advisors just to keep pace. (The Daily Upside)

If they all follow JPM’s path, you get sector-wide margin pressure before any AI payoff shows up. If they don’t, JPMorgan’s moat widens.

Libertarian Lens: Centralized Money, Centralized Costs

From a Libertarian’s perspective, the JPM chart is a side effect of a deeper structural choice.

For fifteen years, central banks suppressed the price of money and underwrote an ever-larger, ever-more-centralized banking system. When capital is cheap and backstops are assumed, scale looks like safety. We built a handful of state-sized banks sitting at the center of the monetary system, layered them with regulation, and implicitly guaranteed them.

Now we’re in a regime of higher rates and stickier inflation. The cost of running those centralized giants has exploded: compliance staff, data centers, AI infrastructure, branches, regulatory overhead. None of that would be this concentrated in a more decentralized, market-driven system.

JPMorgan is doing the rational thing inside the game it’s been given. The uncomfortable truth is that the game itself is centralized money, centralized banking, and centralized regulation make this kind of $105 billion expense base almost inevitable.

If you like smaller, nimbler, more accountable institutions, you don’t get them by accident. You get them by shrinking the footprint of central planners and letting price signals, not backstops, shape the financial system.

Buying Opportunity Or Warning Shot?

Right now, the market is charging JPMorgan a fee for uncertainty. It wants proof that $105 billion in operating expense will translate into sustained high-teens ROE rather than bloated overhead.

If the AI and growth investments drive higher revenue per customer, better risk selection, and stable credit, this week’s candle will age as a temporary air pocket in a long-term uptrend.

If they don’t, the chart you’re staring at is the first honest repricing of a franchise moving from “fortress compounder” toward “expensive utility.”

The number is simple. The consequences are not.

Educational Disclaimer

This article is for educational and informational purposes only and does not constitute investment, legal, tax, or financial advice. Trading and investing in securities, especially when concentrated or using leverage, involves significant risk, including the risk of total loss of capital. Most short-term and active traders underperform passive benchmarks over time. You are solely responsible for your own investment decisions. Always consider your objectives, financial situation, and risk tolerance, and consult a qualified, licensed financial professional before making any investment or trading decisions.

Glossary and Further Reading

Return on equity – A profitability metric that compares a company’s net income to shareholders’ equity.

Efficiency ratio – Common in banking; non-interest expenses divided by net revenue. Lower generally indicates better cost control.

Net interest income – The difference between interest earned on assets (like loans) and interest paid on liabilities (like deposits).

Credit risk – The risk that borrowers fail to make required payments.

Cost of equity – The return required by investors to compensate for the risk of owning a company’s stock.

Exchange-traded fund (ETF) – A pooled investment vehicle that trades on an exchange and typically tracks an index or sector.

Dow Jones Industrial Average – A price-weighted index of 30 large U.S. companies, including major banks.

Federal funds rate – The key U.S. overnight interest rate targeted by the Federal Reserve, influencing borrowing costs across the economy.

AI in finance – A research overview from the Bank for International Settlements on how artificial intelligence is changing financial services.

Risk management – The process of identifying, assessing, and mitigating financial risks within a portfolio or institution.