BTC Playbook x DXY: VWAP Control, Dollar Balance, 24h Outlook

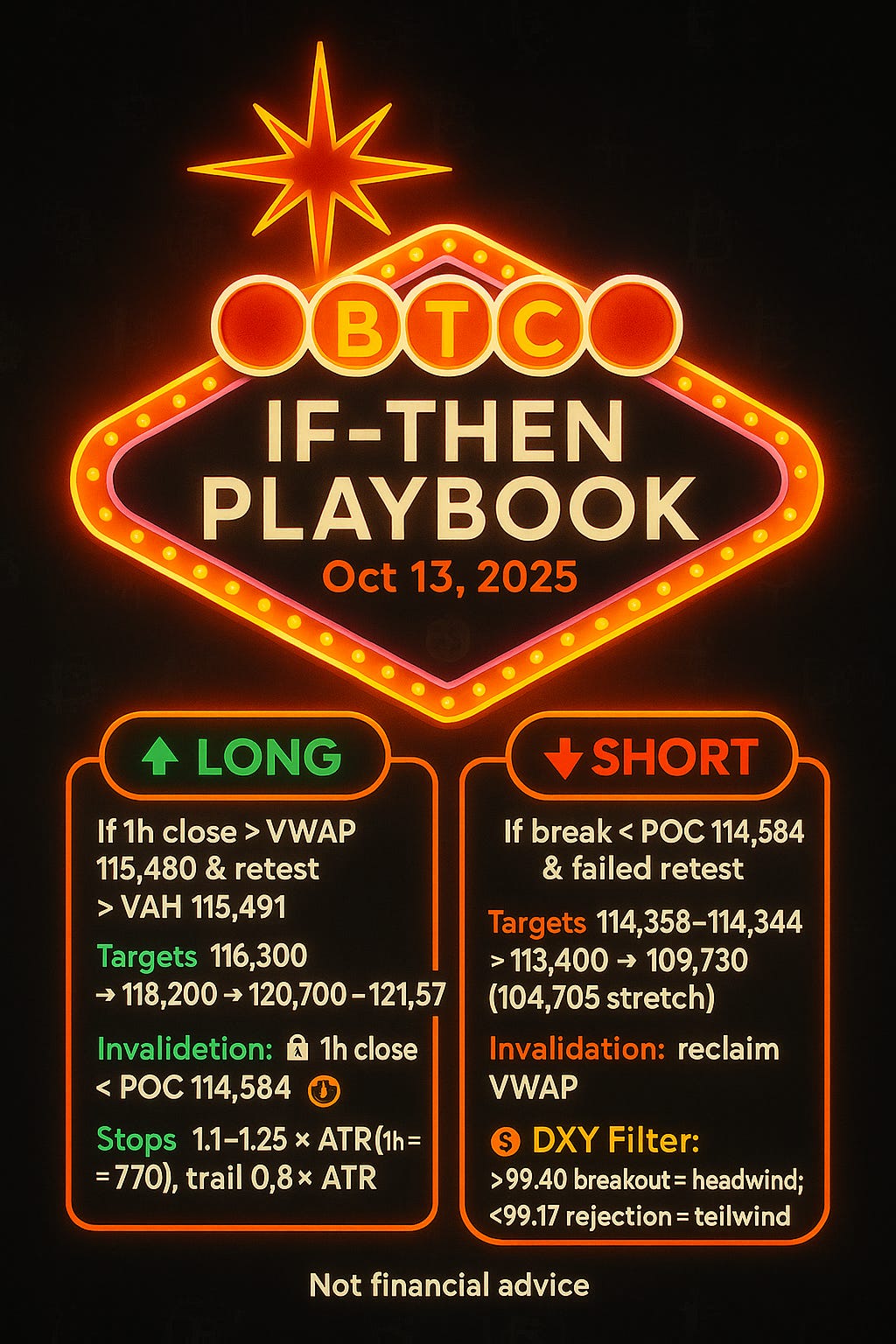

TL;DR: Longs only if BTC accepts > VWAP 115,480 and retests > VAH 115,491.

TL;DR: Longs only if BTC accepts > VWAP 115,480 and retests > VAH 115,491. Shorts on a POC 114,584 break with failed retest. ATR(1h) ≈ 770 for stops. DXY sits in upper-value balance 99.00–99.35; a breakout > 99.40 is a headwind.

Table of Contents

Manager Summary

Maintain range with intraday long bias only on acceptance above VWAP 115,480 and a clean 5–15m retest that holds > VAH 115,491. Short on loss of POC 114,584 with a failed retest. ATR(1h) ≈ 770 governs stops and trails.

Labels: levels = Fact (your screens). Probabilities and path = Theory.

Cross-Asset Snapshot (BTC ↔ DXY)

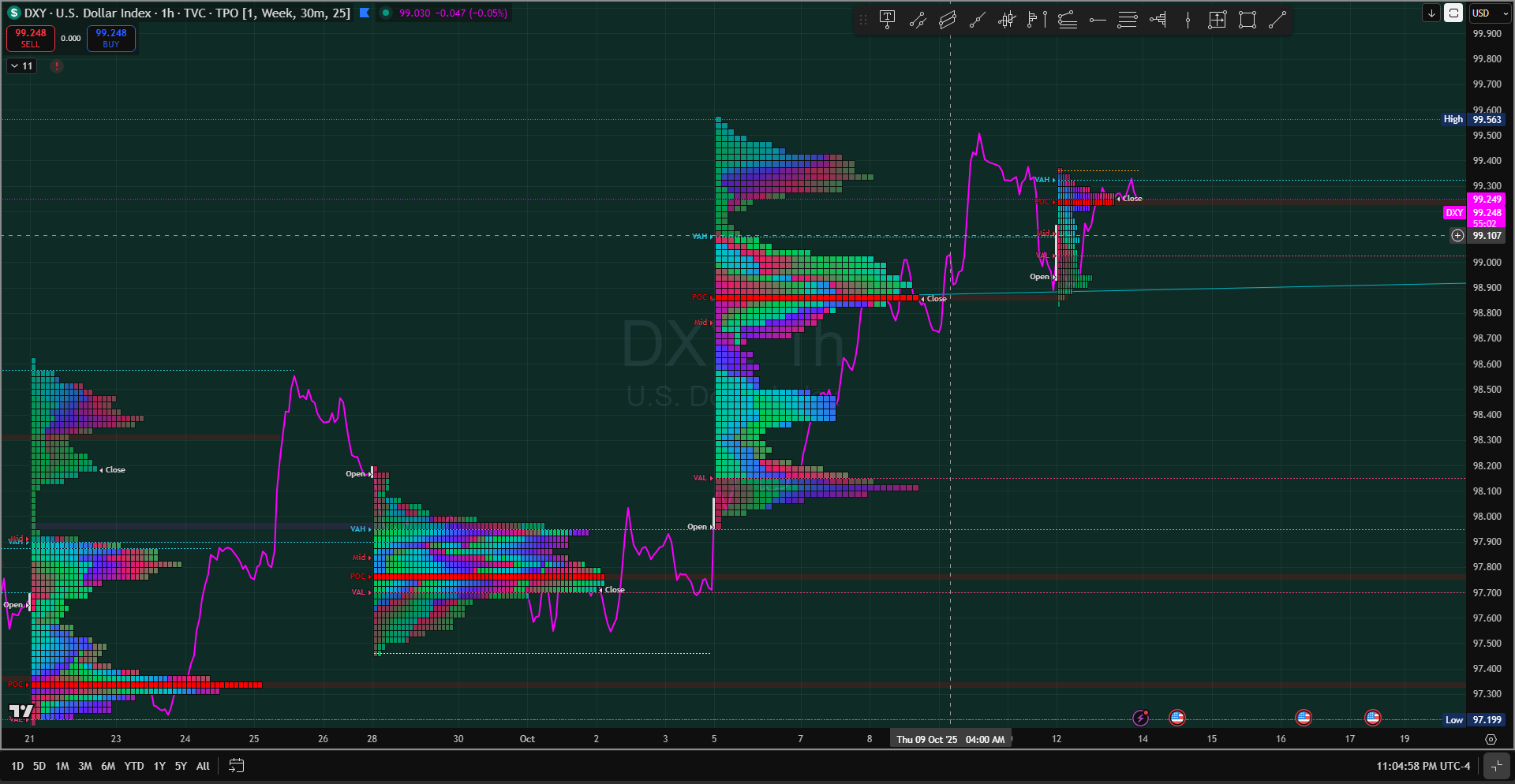

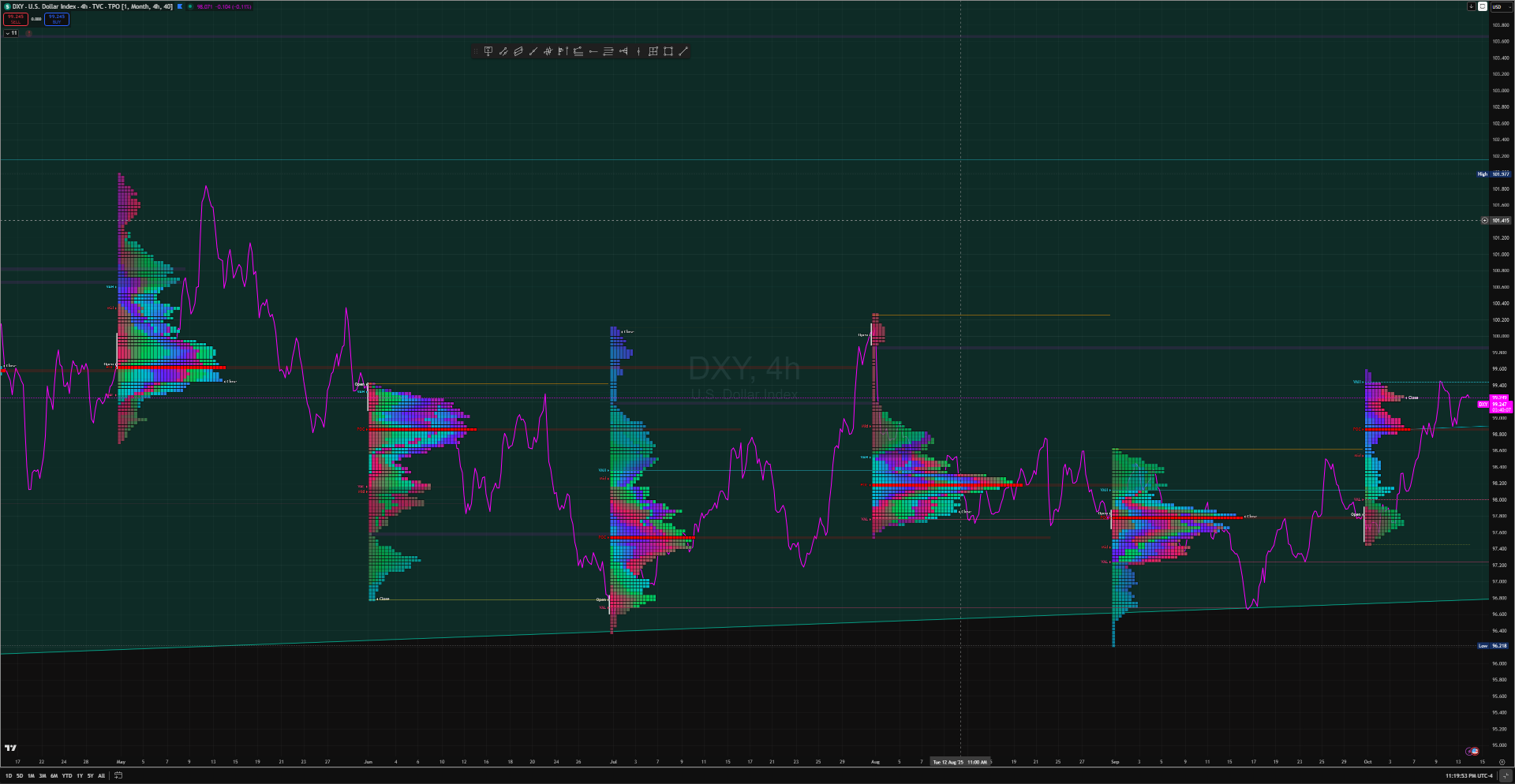

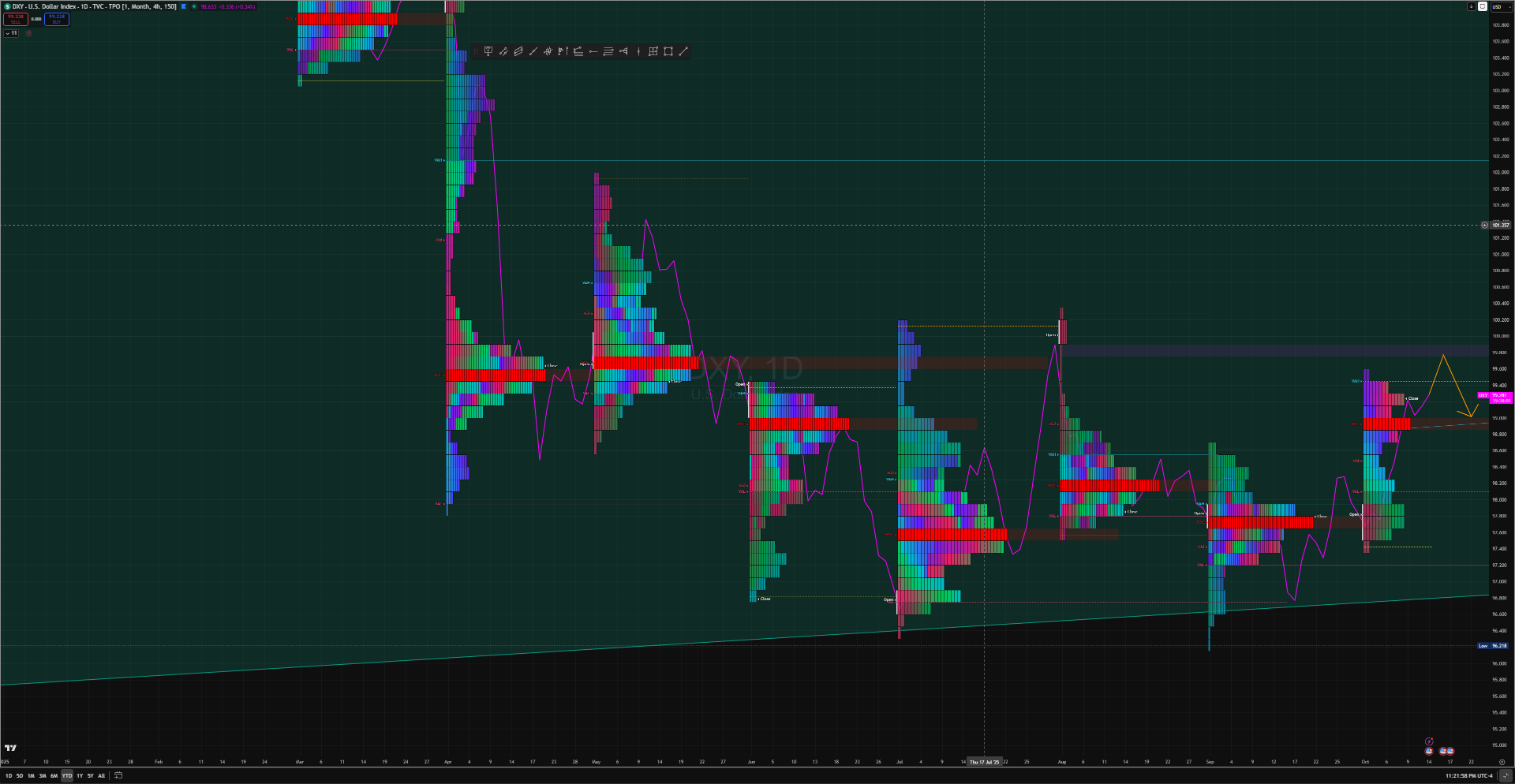

DXY profile (Fact): Weekly composite shows POC 99.17–99.20, VAH 99.35, VAL 99.00, price ≈ 99.26. Upper-value balance after the 97.5 → 99.3 expansion.

Microstructure (Fact): Poor-high clusters 99.35–99.40. Value migrating up on 4h/1D but stalling in the upper third of prior VA.

Inverse link (Fact): 6-week Pearson correlation ≈ −0.74 between BTC and DXY (your calc; definition: Pearson correlation).

Implication (Theory): DXY > 99.40 with value shift up is a BTC headwind. A failure back under 99.17 eases pressure.

If–Then Trade Playbook

Long — If 1h closes > VWAP 115,480 and retest holds > VAH 115,491, then target 116,300 → 118,200 → 120,700–121,257.

Logic: Volume Profile acceptance and Al Brooks measured move projections. (Theory)Short — If clean break < POC 114,584 and failed retest from beneath, then target 114,358–114,344 → 113,400 → 109,730; stretch 104,705.

Logic: rotation back through value; B-shape preference. (Theory)DXY filter — If U.S. Dollar Index > 99.40 with value shift up, favor shorts or stand down on longs until BTC reclaims VWAP. (Theory)

24h Scenario Map

Scenario Condition BTC Bias DXY Expectation Prob (Theory) Plan A. Dollar Breakout ↑ DXY > 99.40 + value shift up To 114.0–113.4k Push to 100.00 43% Short on VWAP failure → POC loss B. Dollar Rejects Upper Value DXY fails > 99.35 and < 99.17 To 116.3–118.2k Rebalance 98.8 39% Long on VWAP retest hold C. Sideways Balance DXY value 99.0–99.3 BTC 115k ± 1k POC dominant 18% Scalp VA edges only Confidence: 58%. Levels = Fact. Weights = Theory.

Core Levels

VWAP: 115,480

VAH: 115,491

POC: 114,584

VAL: 114,358–114,344

Upper test: 120,700–121,257

Lower magnets: 109,730 → 104,705

Why they matter: VWAP benchmark, Value Area/POC, ATR stops. (Fact for tools; Theory for application)

Risk Module

Risk per trade ≤ r%. Daily loss cap.

Stops 1.1–1.25× ATR(1h) beyond invalidation; trail 0.8× ATR after TP1.

Size 0.5× normal while DXY > 99.20; restore full size only if DXY < 99.00.

Halt new entries if BTC and DXY trend in the same direction for > 3 bars. (Uncorrelated break risk)

Quant Firm

Cohorts: profile/TPO, VWAP/execution, price-action (Brooks), Wyckoff, vol/ATR, microstructure, CTA/EMA, options flow, FX/DXY, stat-arb, risk, data QA.

Re-weight with DXY headwind (Fact → your correlation input):

Aggregate BTC Long drops 55% → 52%; Short rises 45% → 48%. Confidence 58%. Notes (Theory): Wyckoff SOS odds lower while DXY balances high; watch poor-high repair at 99.35–99.40 for a binary.

Last Week: What Worked / What To Improve

What worked (Fact/Theory):

Trigger discipline: Best entries aligned with VWAP reclaim + VAH retest before targeting 116.3/118.2.

ATR sizing: Using ATR(1h) for stops avoided noise during mid-value churn.

Avoiding mid-value entries: Fading VA edges inside B-shape sessions reduced chop exposure. We also rode down the Regression trend line as I predicted if price failed to hold on top of the VWAP’s and Monthly Point of Control.

Charts

BTC Hourly VWAP + VAH/POC/VAL → If–Then Trade Playbook

DXY 1H/4H/1D profiles → Cross-Asset Snapshot

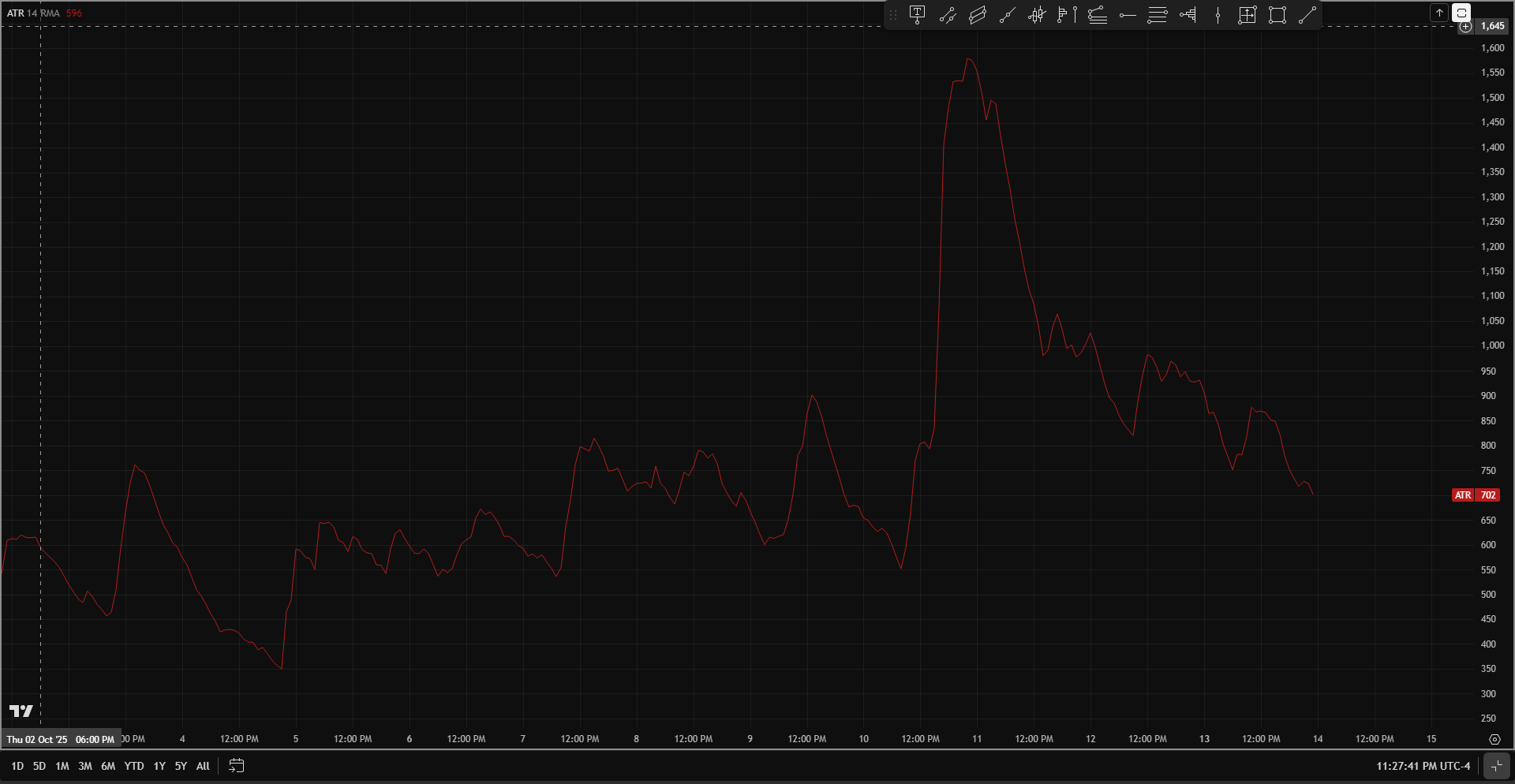

ATR(1h) pane (~770) → Risk Module

One-page beta playbook

Method (Fact): Equal-risk size vs ES1! uses 1M vol from your screen. Multiplier = 0.98% (ES 1M vol) ÷ instrument 1M vol.

Policy filters (Theory):

Risk-off (DXY ≥ 99.20): apply cuts → BTC ×0.50; NQ ×0.70; ES ×0.80; low-beta stocks ×0.70; mid-beta ×0.50; high-beta (β≥1.5 or 1M vol ≥5%) ×0.30.

Risk-on (DXY < 99.00): use equal-risk size (no cut).

Bonds (ZB1): as ballast use ×1.20; otherwise ×0.80.

How to use:

Pick the final size from the column matching the DXY regime.

Apply your standard risk per trade r%.

Stops remain 1.1–1.25 × ATR(1h ≈ 770); trail 0.8 × ATR after TP1.

Fact/Theory audit: Vol and betas = Fact from your screenshot. Multipliers = Fact from formula. Risk-off cuts and bond ballast factors = Policy/Theory aligned to your regime rules.

Disclaimer

Educational only. Not financial advice. Most day traders lose money. Do your own research and consult a licensed professional.

If you want to try your hand at videos like this please use my referral link for Neural Frames